Supply Chain & Sourcing Updates Q3 2026

Material Matters is Taylor’s quarterly research report analyzing supply chain conditions, sourcing trends and marketing pricing print, direct mail, packaging, and physical marketing materials.

Table of Contents

Q3 2026 Market Trends and Economic Indicators

The ISM manufacturing PMI index registered 54% in May 2026, marking strongest U.S. factory growth in four years.

New orders, backlogs and production continued to grow, while raw materials and finished goods inventory contraction slowed. Price index decreased slightly (2.5%) in May versus April, but still remains high versus the previous year.

Consumer Spending/Sentiment

Consumer sentiment has rebounded significantly in Q2 2026 versus Q1 2026 as gasoline prices moderated. U.S. consumer spending has remained resilient, rising by 0.7% even with inflation increasing to an annual rate of 4.2%.

Commodity Pricing

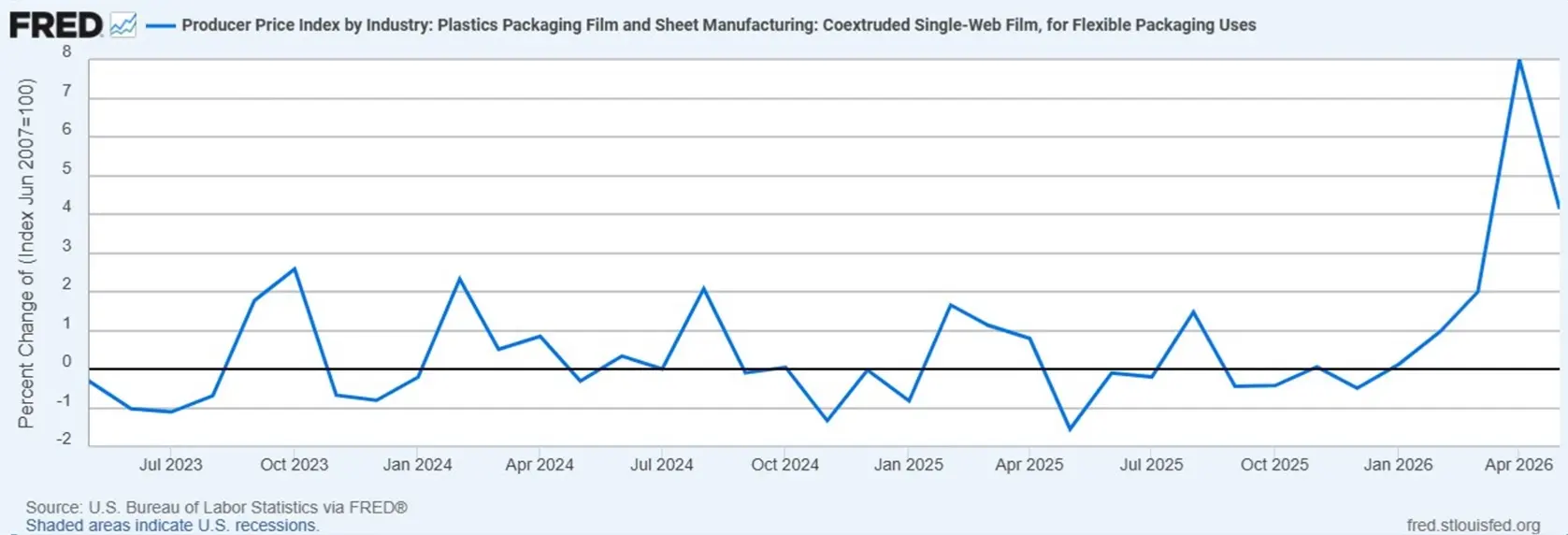

Multiple commodities pricing increased in May, including metals, chemicals, plastics, paper, packaging, electronics, MRO supplies and energy inputs. Gasoline, diesel and crude oil continue to be at elevated levels due to the Middle East conflict.

Energy

WTI crude oil, U.S. diesel and gasoline prices have declined slightly from the significant spikes in Q2 due to the continued Middle East conflict. Fuel prices are expected to decrease in Q3 while domestic natural gas and consumer electricity rates are expected to increase.

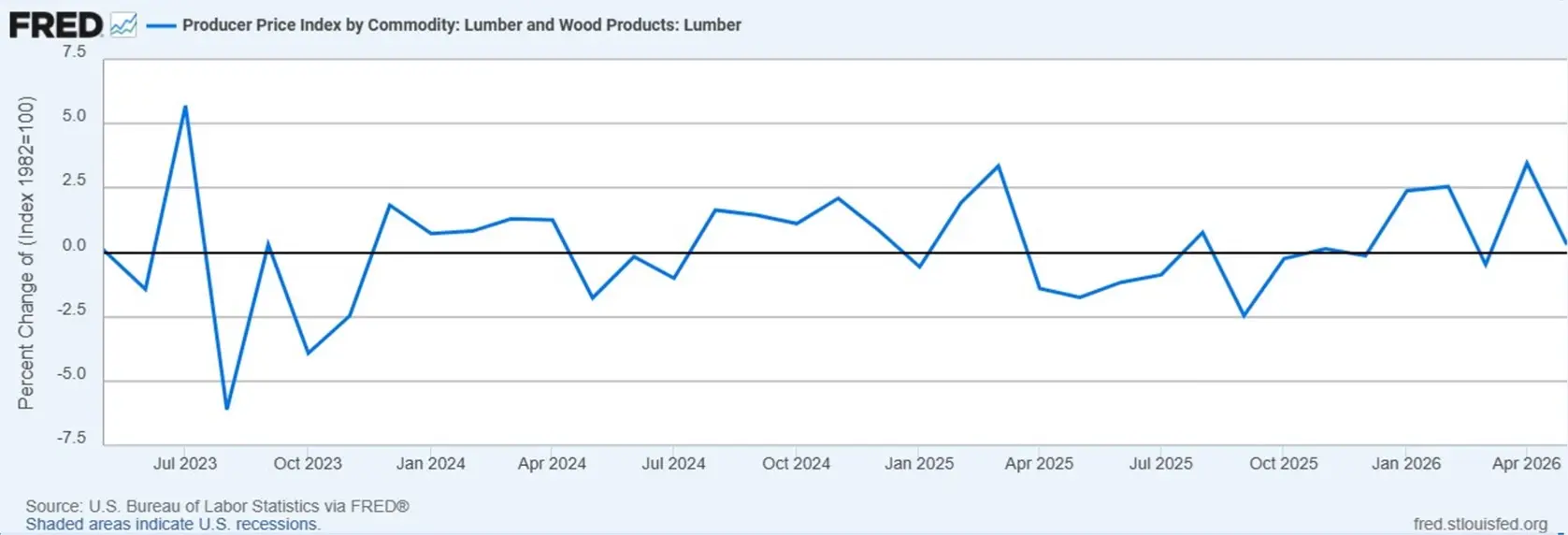

Paper Facestocks and Liners

- Paper label facestock and liner material pricing continued to increase in Q2 and is expected to have negative impact in Q3 2026. As previously reported, paper mills are moving toward higher-value products and consolidating. Although paper facestock supply is relatively stable, there are signs that certain types of liner product supply is tightening and/or longer lead times are being implemented.

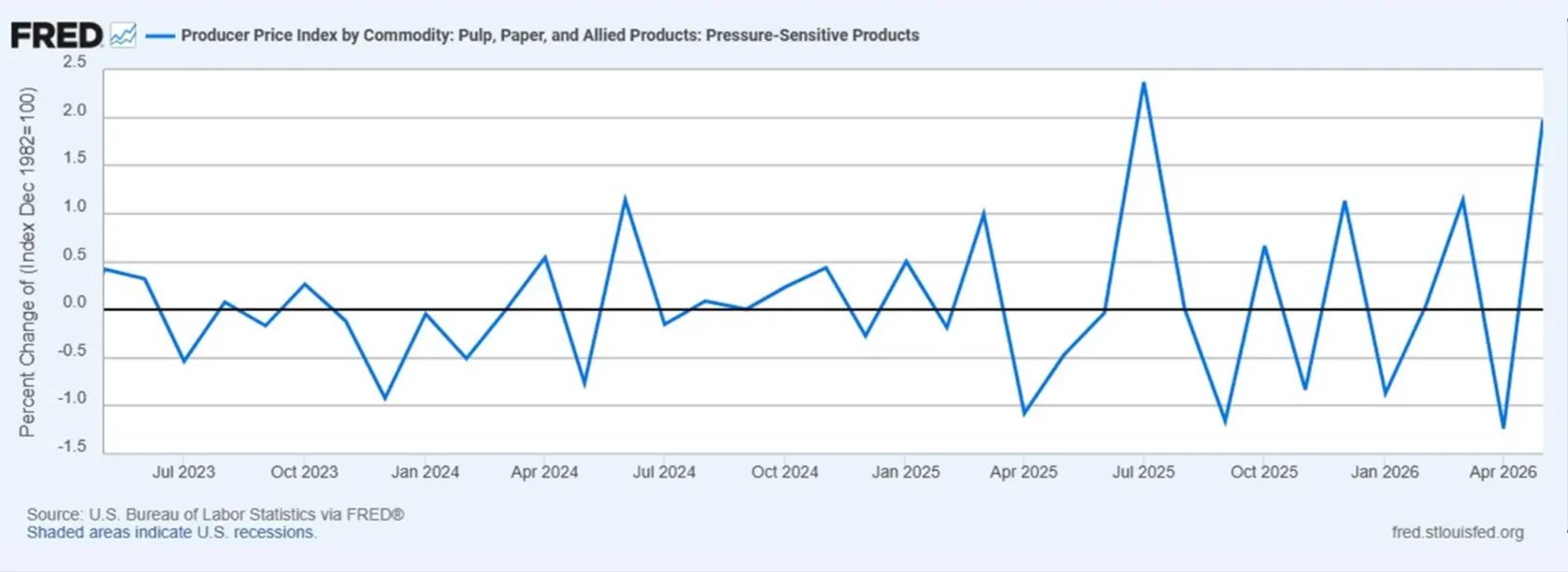

Labels PPI

The graph below details the Producer Price Index (PPI) for raw label pressure-sensitive materials from May 2023 through May 2026.

NOTE: New quarterly data not available until mid-to-late July 2026.

Aluminum & Tooling/Die Categories

- Aluminum pricing increased in February 2026 with tariffs continuing to pressure the market. Aluminum costs are having the greatest impact on CTP equipment.

- Processless plates continue to be a rising trend in the overall plate-making market.

- Demand for aluminum plates is growing moderately and is expected to continue into 2027.

- Tooling and die markets have implemented price increases and tariff surcharges driven by higher material costs and trade policy changes.

Half-Year Growth in Focus

Promo closed 2025 at a record $27.7 billion, growing 4.2% and outpacing the broader U.S. economy, but momentum cooled

entering 2026 as tariffs and geopolitical costs weighed on demand.

Van Demand & Capacity

Van Load-to-Truck Ratio

International Logistics Market Rate Per Full Container Unit

Fall Season Importing

US imports from Asia in May jumped to 1.68 million TEUs, up 13% from April, almost 20% higher year over year, and the highest since last August, according to PIERS (an import/export database).

The National Retail Federation (NRF) has upgraded its forecast for June imports, confirming peak season has come early this year. NRF expects it to be lower through the rest of the summer into early fall.

Source: Journal of Commerce

%20Market%20Overview/International-Market-Overview.webp)