Material Matters from Taylor - Q1 2026

Your quarterly update on the latest sourcing trends, market pricing and the overall state of supply chains.

Table of Contents

Q1 2026 Market Trends and Economic Indicators

Institute of Supply Chain Management (ISM) manufacturing PMI index finished at 47.9% in December 2025. This represents the 10th straight month of manufacturing sector contraction.

New orders, backlogs, production and raw material inventories all contracted at slower rates while overall prices continue to remain stable from previous months. The index still points to growth in the U.S. economy (GDP increased to 4.3% for Q3 2025) primarily driven by consumer spending, exports and government spending despite manufacturing contraction.

Consumer Spending/Sentiment

Consumer sentiment continued to decline for the second month in a row. The University of Michigan's Index of Consumer Sentiment increased slightly to 52.9 in December 2025 from the previous month.

Expectations are that consumer sentiment will remain same going into Q1 2026. Primary drivers for little-to-no change include higher consumer goods and services prices, pessimism about the labor market, higher out-of-pocket healthcare costs, and strained household budgets/income.

Commodity Pricing

Commodity pricing is mixed among heavy metals, chemicals, plastics, packaging and energy components with aluminum, steel, copper, natural gas, paper products and electronic components seeing higher rates of increasing prices.

Standard gasoline, oil and polypropylene resin are all seeing lower pricing. The U.S. tariff policy remains a focus for both manufacturers and consumers. (See Imports section for more details.)

Energy

WTI crude oil, U.S. diesel fuel and standard gasoline are all expected to continue to be lower and/or flat in Q1 2026. This is primarily driven by lower WTI (U.S.) and Brent Crude (global) oil prices due to lower demand and higher production and inventories.

Natural gas pricing is expected to remain stable at $4/MMBTU. Keep in mind that the current situation in Venezuela should have limited impact on oil pricing with the current global surplus and OPEC production strategy.

Printing and Writing Papers

Neenah, Mohawk, Pixelle and Sylvamo announced price increases effective Q1 2026.

Shutdowns contributed to significant shifts in the uncoated paper market in 2025 and these will continue to be felt in 2026.

Price Increases

Neenah and Mohawk appear to be making standard annual increases, while Pixelle’s price increases reflect their ongoing instability following the Chillicothe, OH, plant shutdown and continued restructuring.

Uncoated Paper

Q1 2026 is expected to see tighter supply and additional price increases in the uncoated paper market, primarily due to overall industry capacity reductions, such as Sylvamo’s Rivervale mill closure and Pixelle’s planned pulp mill shutdown in March 2026.

Tariff Impact

Tariffs implemented in 2025 will also impact the paper industry going into 2026. Maintaining strong relationships with preferred mill partners will be essential for supply continuity during these market disruptions.

North American Coated Coated Freesheet Operating Rates

North American Uncoated Coated Freesheet Operating Rates

Paper Facestocks and Liners

- Thermal paper and paper liner material supply and demand remain balanced with continued emphasis on CA Prop 65 and WA Phenol-Free product requirements. There is potential for upstream paper mill consolidation and/or planned shutdowns in favor of higher value products.

- Global supply and lead times on standard products are expected to remain stable with longer lead times for specialty paper-based label materials.

- Platinum prices continue to hit all-time highs surpassing $2,000/ounce. It is expected that platinum prices will push even higher in 2026 due to operational disruptions and rising mining costs. Ultimately, platinum pricing will put pricing pressure on silicones used for label liner manufacturing costs in 2026.

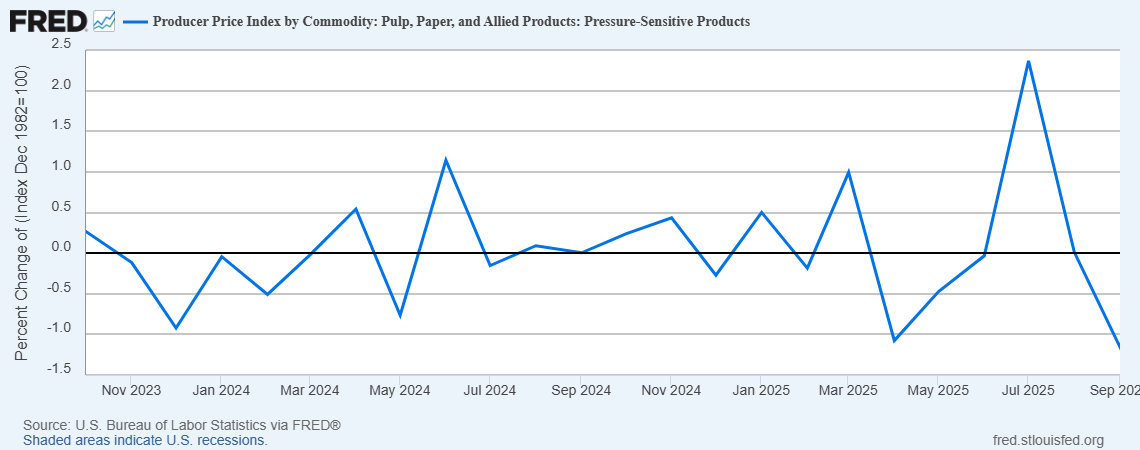

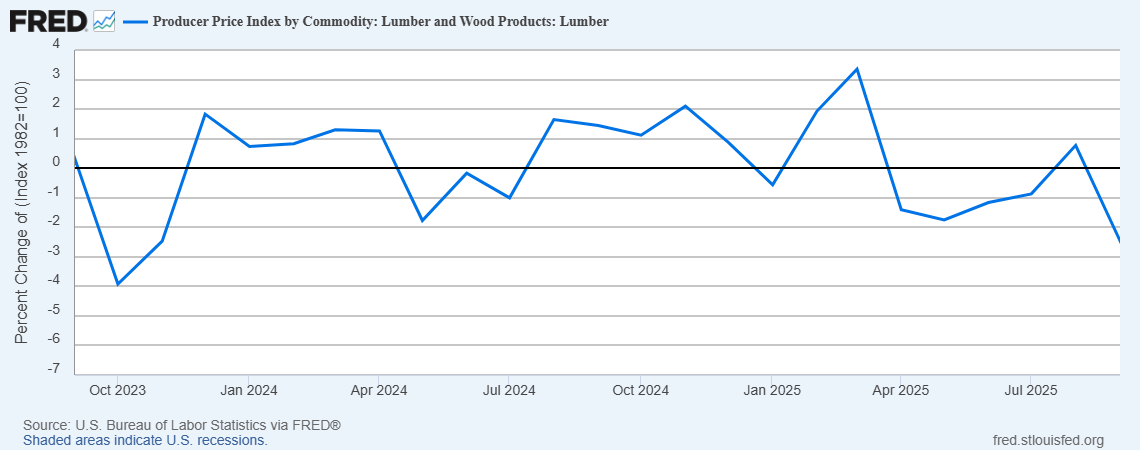

Labels PPI

The graph below details the Producer Price Index (PPI) for raw label pressure-sensitive materials from September 2023 through September 2025.

**NOTE** New quarterly data not available until mid-to-late January 2026.

Aluminum & Tooling/Die Categories

- Aluminum material pricing is expected to remain stable through Q1 2026, but tariffs are significantly impacting CTP equipment, with aluminum raw materials continuing to be the most affected.

- Processless plates continue to be a rising trend in the overall plate making market.

- Aluminum plates are showing moderate growth and expected to continue into 2027.

- Tooling and die markets have implemented price increases and/or tariff surcharges, driven by both material costs and trade policy shifts.

Driving Responsibility

PPAI Media takes a look at how sustainability and compliance took center stage for promo in 2025.

State of the Industry

ASI's Counselor State of the Industry Report details promo sales, tariffs, tech and market trends from 2025.

Top 10 Trends of 2025

PPM provides analysis and commentary on the top trends in promotional marketing over the past year.

Small Package Market Overview

The small parcel shipping market faces a complex landscape of ample capacity and soft demand, with carriers employing aggressive strategies to offset volume challenges through pricing mechanisms.

Carrier Capacity

Major carriers (UPS, FedEx, DHL, USPS) are expected to have stable capacity, but last-mile congestion will continue due to holiday season spillover and same-day delivery demand.

Carriers continue to invest in AI-driven technology for route and load optimization, micro-fulfillment hubs, and enhanced real-time shipment visibility.

Pricing Strategies

Q1 2026 will continue to see General Rate Increases (GRI) averaging 7%–12%:

UPS

5.9% effective 12-22-25

FedEx

5.9% effective 1-5-26

DHL

5.9% effective 1-1-26

USPS

7.8% GA

6.6% Priority effective 1-18-26

Shippers are expected to reassess packaging and carrier mix to help offset additional logistics costs.

Outlook

Shippers must continually evaluate packaging and service level mix, have strong strategic relationships with carrier partners and leverage technology platforms (e.g., AI; TMS).

Less-Than-Truckload Logistics Market Overview

The North American LTL market enters Q1 2026 with greater stability than in 2025, but continues to feel the effects of changes across the freight ecosystem. LTL market conditions remain consistent with late 2025, reflecting a soft domestic freight environment and muted economic activity.

The LTL market is expected to impacted less by sudden demand spikes and more by structural constraints, including tighter capacity, compliance pressures and evolving cross-border freight movement, especially with Mexico. Although LTL freight volumes remain below pre‑pandemic levels, modest recovery continues in sectors tied to industrial production and cross‑border trade, aligning with early 2026 freight stability indicators.

Carrier Capacity

Capacity remains tight, primarily due to continued freight volume being redistributed after previous carrier consolidation and/or complete exiting from the market. Fewer drivers and constrained network flexibility within specific North American regions has also contributed to forecasted LTL capacity trends in 2026.

Pricing Strategies

LTL rate pressures are expected to persist into Q1 2026. While contract rates remain relatively steady, accessorials and surcharges — especially fuel‑related and service‑specific fees — are increasing, consistent with broader transportation cost inflation trends. Read more about the LTL landscape at mynatsa.org.

Outlook

Shippers must prepare for continued rate pressure, tight capacity and longer lead times. Strategic carrier selection, technology adoption and flexible routing will be key to maintaining service levels. The Taylor sourcing team will continue to align with reliable LTL partners to support business needs through Q4 2025 and into 2026.

Van Demand & Capacity

Van Load-to-Truck Ratio

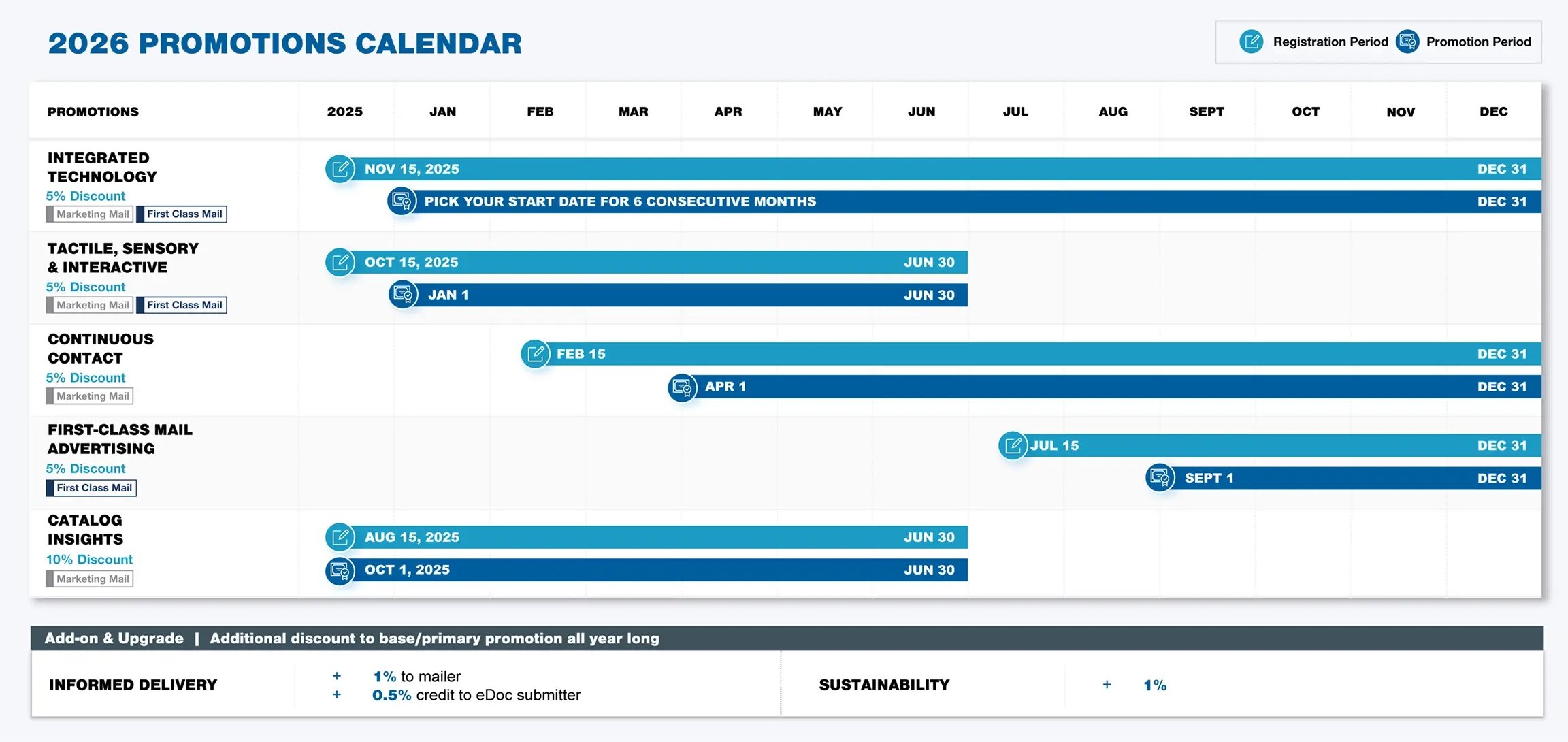

Reminder: New 2026 Promotions

- Registration for catalog insights was effective as of Aug. 15, 2025. Tactile, sensory and interactive promotion registration started Oct. 15, 2025.

- All the New 2026 Promotions: 2026 Promotions Guidebooks | PostalPro

U.S. - Mexico - Canada Free Trade Agreement (USMCA)

Potentially the most important trade policy news this year will be the outcome of negotiations over the United States-Mexico-Canada Agreement (USMCA).

In December, U.S. Trade Ambassador Jameson Greer briefed Congress on the administration's goals and positions heading into the six-year review of the trade deal.

While Greer did not explicitly commit to renewing the USMCA and indicated that the United States would negotiate aggressively during this process, the administration has indicated it favors nearshoring in North America over other alternatives.

%20Market%20Overview/International-Market-Overview.webp)

U.S. Supreme Court Final IEEPA Ruling

Upcoming Decision

Analysts have been waiting for a ruling on the U.S. Supreme Court IEEPA tariffs case, with many expecting it to come by the end of January 2026.

Possible Effects

The decision is one of the most anticipated events of the year, as it could create refunds for importers, raise questions about the preliminary trade pacts the U.S. has struck and renew concerns about the fiscal deficit.

Budget Office Estimate

The tariffs are expected to subtract $3 trillion from the deficit over 10 years, according to the latest Congressional Budget Office estimate. The Yale Budget Lab estimates about half of the new tariff revenue comes from IEEPA tariffs.

%20Market%20Overview/Tariff-Mitigating-Strategies.webp)