Q2 2026 Supply Chain & Procurement News

Material Matters from Taylor is your quarterly update on the latest sourcing trends, market pricing and the overall state of supply chains.

Table of Contents

Q2 2026 Market Trends and Economic Indicators

Institute of Supply Chain Management (ISM) manufacturing PMI index registered 52.4% in February 2026, marking the 16th straight month of expansion.

New orders, backlogs and production continued to grow, while raw materials and finished goods inventories contraction slowed. Prices surged to 11.5% (highest since June 2022). Overall the PMI Index continued to signal U.S. economic growth, primarily driven by AI investment, fiscal policy and tax incentives, easing monetary and tariff policy, resilient consumer spending, and manufacturing exports.

Consumer Spending/Sentiment

Consumer sentiment weakened significantly by late Q1 2026, reaching its lowest level since December 2025. Elevated fuel prices, inflation expectations and geopolitical risk from the Middle East conflict were primary drivers. Q2 2026 consumer spending is expected to remain soft with continued pressure on discretionary goods and services such as travel, dining and entertainment.

Commodity Pricing

Commodity pricing remains mixed with upward pressure across metals, chemicals, plastics, paper, packaging, electronics and energy inputs. Gasoline, diesel fuel and crude oil prices spiked sharply during end of Q1 2026 and into Q2 2026 largely due to the Middle East conflict. The U.S. tariff policy remains a consideration following the Supreme Court overturning the IEEPA specific tariffs. (See Imports section for more details.)

Energy

WTI crude oil, U.S. diesel, and gasoline prices have deviated sharply away from Q1 2026 projections, primarily driven by the Middle East conflict. Energy prices are expected to remain elevated through at least early Q2 2026. S&P Global and the OECD agree the current inflation spike is supply‑driven rather than demand‑led, reducing the risk of runaway inflation. However, price normalization is likely to take additional time during Q2 2026.

North American Uncoated Free Sheet Capacity

North American Uncoated Free Sheet Share

North American Coated Free Sheet Capacity

North American Coated Free Sheet Share

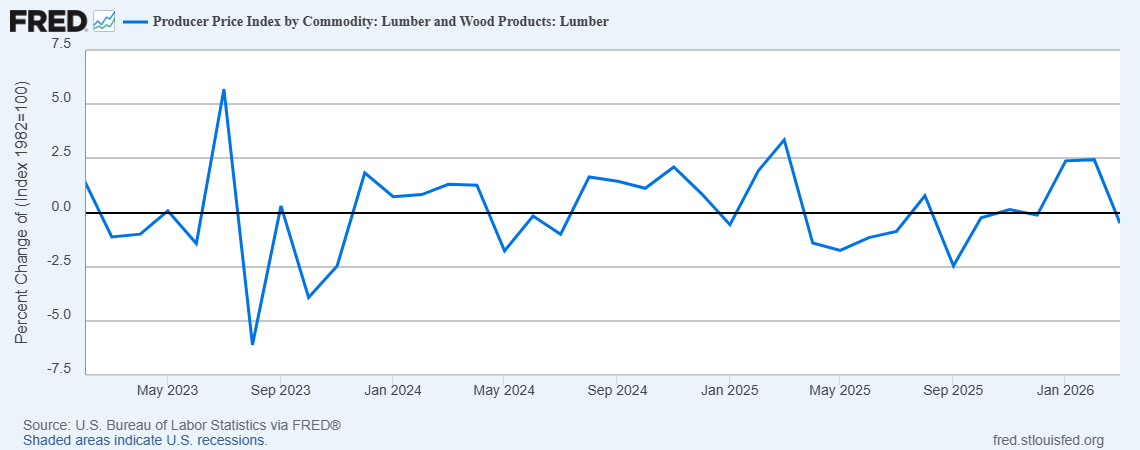

Paper Facestocks and Liners

- Thermal paper label facestock and paper liner materials supply is expected to be stable, but there is still pressure from the upstream paper mills.

- Pressures include mills continuing to move away from commodity paper products in favor of higher value products, further operations consolidation across NA and Europe, and/or additional paper mills being closed altogether.

- Global demand is expected to remain fairly stable with nominal growth.

- Platinum prices continued to climb to another all-time high of $2,800/ounce in mid Q1 2026. Pricing in Q2 2026 is expected to remain fairly stable, remaining closer to $2,000/ounce. These increases in platinum pricing are forcing increases in silicones used for label liner manufacturing costs.

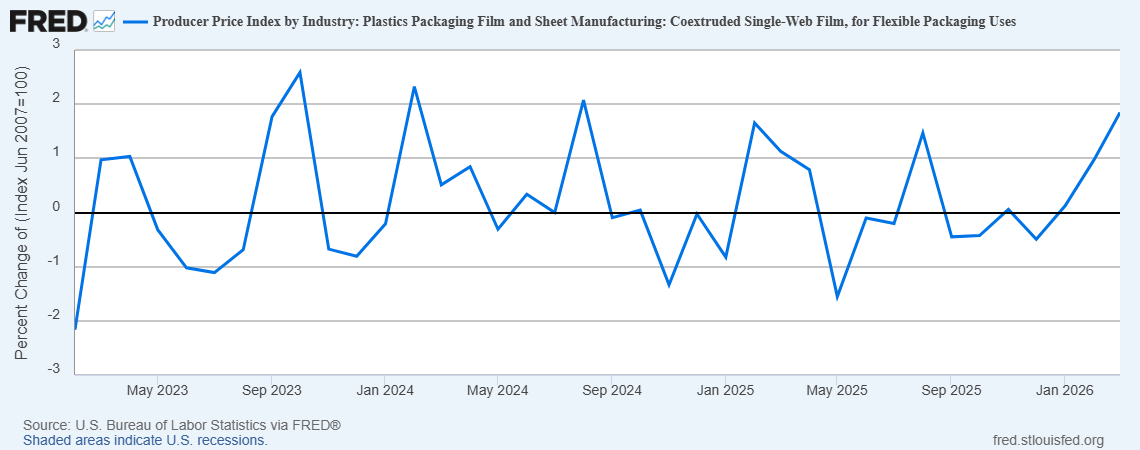

Labels PPI

The graph below details the Producer Price Index (PPI) for raw label pressure-sensitive materials from February 2023 through February 2026.

NOTE: New quarterly data not available until mid-to-late April 2026.

Aluminum & Tooling/Die Categories

- Aluminum material pricing increased in February 2026 with tariffs continuing to pressure the market. Aluminum costs are having the greatest impact on CTP equipment.

- Processless plates continue to be a rising trend in the overall plate-making market.

- Demand for aluminum plates is growing moderately and is expected to continue into 2027.

- Tooling and die markets have implemented price increases and tariff surcharges driven by higher material costs and trade policy changes.

Van Demand & Capacity

Van Load-to-Truck Ratio

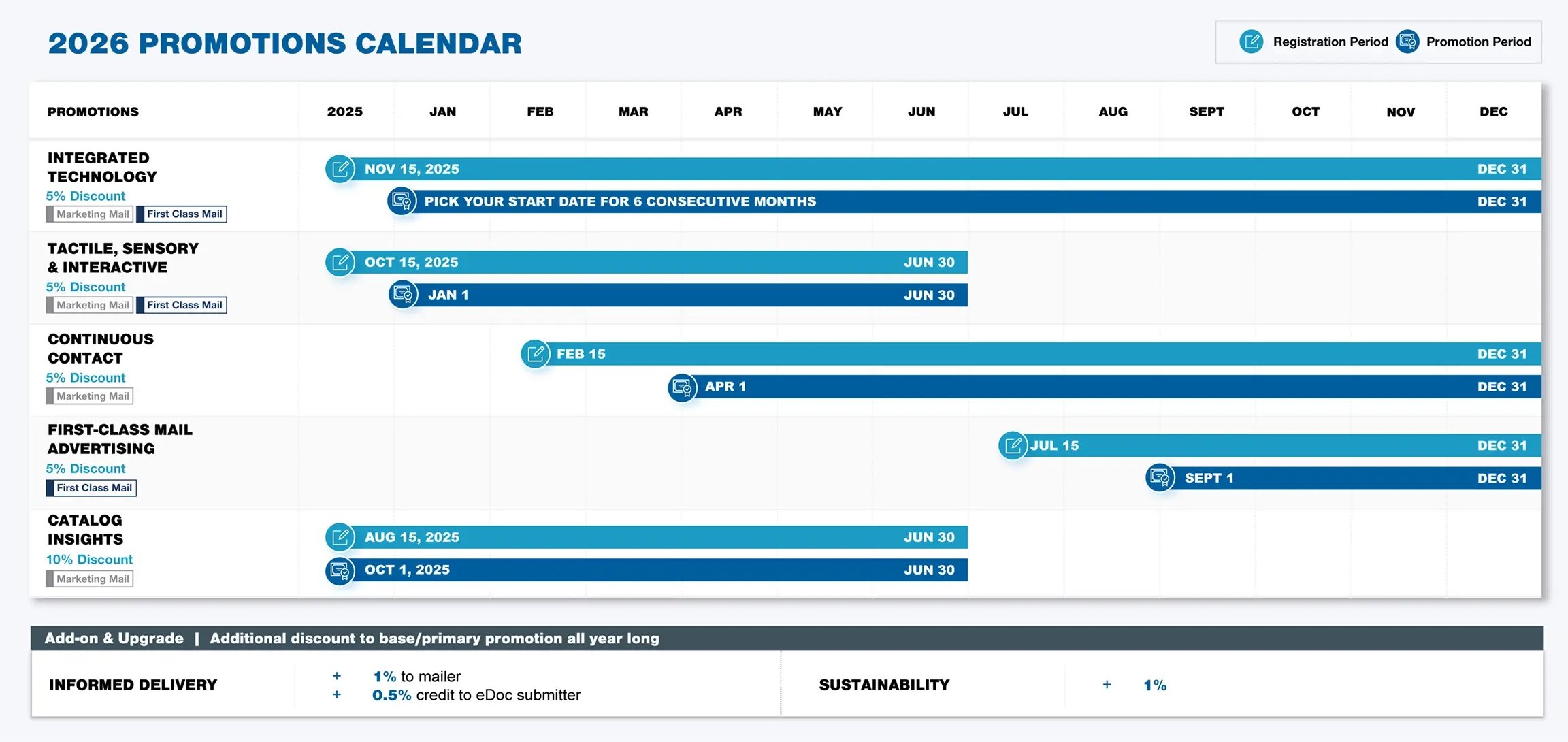

Reminder: New 2026 Promotions

- Registration for catalog insights was effective as of Aug. 15, 2025. Tactile, sensory and interactive promotion registration started Oct. 15, 2025.

- All the New 2026 Promotions: 2026 Promotions Guidebooks | PostalPro

State of IEEPA Tariff Refunds

What did the Supreme Court decide about IEEPA tariffs?

The Supreme Court held that the International Emergency Economic Powers Act (IEEPA) does not authorize the

President to impose tariffs. The majority focused on statutory text, noting Congress did not expressly grant tariff-imposition authority under the IEEPA.

%20Market%20Overview/International-Market-Overview.webp)