Material Matters from Taylor - Q4 2025

We want to keep our partners in the loop regarding the latest sourcing trends, market developments and the overall state of supply chains today.

That’s why we created Material Matters.

Table of Contents

Q4 2025 Market Trends and Economic Indicators

Institute of Supply Chain Management (ISM) manufacturing PMI index finished at 49.1%for September 2025 indicating contraction in manufacturing.

That said, September PMI index is a slight increase from August 2025 and a 2% increase from September 2024. New orders, backlogs, production and raw materials inventories all contracted at varying rates while overall prices continue to remain higher. Index still points to growth in the U.S. economy (GDP increased to 3.8% for 2nd Qtr 2025) despite manufacturing contracting.

Consumer Spending/Sentiment

Consumer sentiment continued to decline for second month in a row. The University of Michigan's Index of Consumer Sentiment declined to 55.1 in September, a 3.1 decrease from previous month. Primary drivers include: higher prices; pessimism about labor market and the softening of personal income.

Commodity Pricing

Commodity pricing is mixed among heavy metals, chemicals, plastics, packaging and energy components with aluminum, copper, corrugated packaging, paper products and electronic components seeing higher rates of increasing prices. The U.S. tariff policy remains a focus for manufacturers, and ultimately for consumers. (See Imports section for more details.)

Energy

WTI crude oil, U.S. diesel fuel and standard gasoline are all expected to continue to be lower and/or flat for the remainder of 2025 as well as into early 2026. This is primarily driven by lower WTI oil prices due to lower demand and higher production and inventories. Natural gas pricing is expected to increase due to higher global demand.

Mill Shutdowns & Conversions

August saw an acceleration in mill closures and conversions. These closures represent “the largest downward capacity adjustment ever" according to Fastmarkets.

International Paper (IP)

International Paper (IP) sold its pulp business and converted 260K tons of white cut stock into 430K tons of containerboard. It also shut down two container board mills totaling 1.4M tons of capacity.

Pixelle & Domtar

Pixelle completed the shutdown of its Chillicothe mill on August 10, while Domtar closed 235K tons of newsprint capacity, representing 10% of North America's total.

Other Closures

More notable closures in 2025 include UPM, Willamette Falls, Irving Paper, Greif and Cascades.

Elutia Bioevenlope Sale to Boston Scientific

October 1, 2025, Elutia announced the successful closing of an $88 million sale of its bioenvelope technologies to Boston Scientific, focusing on the advancement of drug-eluting biologics for medical devices.

Pidgeon Envelope Facing Foreclosure

Major Ohio-based envelope manufacturer, Pidgeon Envelope LLC (parent of Envelope 1 LLC) is facing court-ordered foreclosure and sheriff's sale due to outstanding debt payments.

Innovations in Interactive Envelopes

Envelope manufacturers are incorporating augmented reality and near-field communication RFID NFC technology into envelopes, transforming them into interactive marketing tools that offer digital content and memorable brand experiences.

North American Coated Freesheet Operating Rates

North American Uncoated Coated Freesheet Capacity and Demand

Paper Facestocks and Liners

- Thermal paper and paper liner material supply and demand remains balanced with continued emphasis on CA Prop 65 and WA Phenol-Free product requirements.

- Global supply and lead times on standard products are expected to remain stable with longer lead times for specialty paper-based label materials.

- Platinum prices continue to soar, hitting an all-time 12.5 year high, surpassing $1,600/ounce. Driven by a strong rally since April 2025, platinum significantly outperformed gold and silver, which is expected to have some effect on silicone liner manufacturing costs in Q4 2025/early 2026.

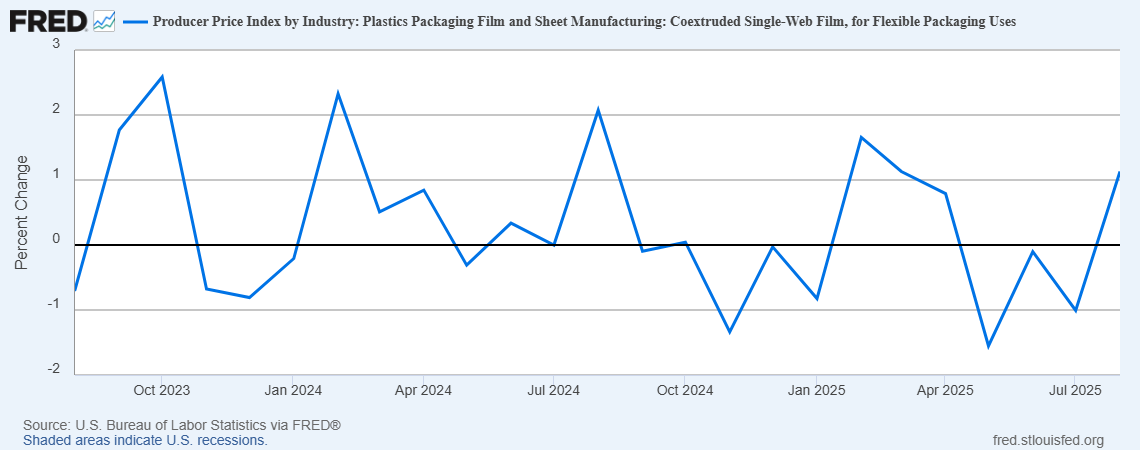

Labels PPI

The graph below details the Producer Price Index (PPI) for raw label pressure-sensitive materials from August 2023 through August 2025.

Aluminum & Tooling/Die Categories

- Aluminum material pricing is expected to remain stable through Q4 2025, but tariffs are significantly impacting CTP equipment, with aluminum raw materials continuing to be the most affected.

- Tooling and die markets have implemented price increases and/or tariff surcharges, driven by both material costs and trade policy shifts.

Promotional Product Momentum

What are the best promotional trends of 2025? EverythingBranded has your answer.

Put School Pride To Work With Promo

See the growth in school-themed merchandise.

Tariff FAQs

Taylor Promo Products Provides FAQs to Current Tariff Challenges

Small Package Market Overview

The small parcel shipping market faces a complex landscape of ample capacity and soft demand, with carriers employing aggressive strategies to offset volume challenges through pricing mechanisms.

Carrier Capacity

Major carriers (UPS, FedEx, DHL, USPS) maintain stable capacity, but last-mile congestion and urban delivery bottlenecks are emerging as peak season ramps up. Infrastructure investments continue to support volume surges, though cross-border shipments face compliance challenges.

Pricing Strategies

Q4 2025 sees continued rate pressure with USPS, FedEx and UPS implementing general rate increases (5.9%) and peak season surcharges. Dimensional weight pricing and residential delivery fees are up over 25%, prompting shippers to reassess packaging and carrier mix.

Outlook

Shippers must stay agile, leveraging technology, blended carrier strategies and service level audits to manage rising costs and maintain delivery performance. The Taylor team will continue to align with optimal logistics partners to support business needs through the holiday surge and into 2026.

Less-Than-Truckload Logistics Market Overview

The North American LTL market enters Q4 2025 in a rebalancing phase, following the closure of Yellow Corporation and ongoing carrier consolidation.While freight volumes remain below pre-pandemic levels, signs of recovery are emerging, driven by industrial manufacturing, nonresidentialconstruction, and cross-border trade with Mexico. Infrastructure investments and regulatory changes are reshaping inland networks and customsprocesses, requiring shippers to stay proactive.

Carrier Capacity

Capacity remains tight due to reduced competition and redistributed freight from Yellow’s exit. Major carriers like FedEx Freight and XPO are expanding service areas and investing in automation, but regional bottlenecks and longer transit times persist in some lanes.

Pricing Strategies

Rates are increasing steadily, with Q4 seeing higher surcharges for expedited and specialized services. Fuel costs remain elevated, and AI-driven freight management systems are being adopted to optimize pricing and routing.

Outlook

Shippers must prepare for continued rate pressure, tight capacity and longer lead times. Strategic carrier selection, technology adoption and flexible routing will be key to maintaining service levels. The Taylor sourcing team will continue to align with reliable LTL partners to support business needs through Q4 2025 and into 2026.

Van Demand & Capacity

Van Load-to-Truck Ratio

New USPS 2025 and 2026 Promotions

- Registration for catalog insights was effective as of Aug. 15, 2025. Tactile, sensory and interactive promotion registration started Oct. 15, 2025.

- All the New 2026 Promotions: 2026 Promotions Guidebooks | PostalPro

Supreme Court Agrees to Review IEEPA Tariffs

The U.S. Supreme Court agreed to review whether the International Emergency Economic Powers Act authorizes

the president to impose tariffs via executive order. The case will be heard on an expedited schedule, most likely during the first week of November (3, 4 or 5).

If Supreme Court upholds the President's tariffs, that is the end of the judicial challenges to tariffs and there would be no refunds.

%20Market%20Overview/International-Market-Overview.webp)

Tariff Mitigating Strategies

Diversifying Country of Origin

Sourcing from other countries least impacted by tariffs.

Tariff Engineering

Designing the product to fit into the appropriate product classification based on HTS (Harmonized Tariff Schedule).

Understanding Free Trade Agreements

Including regional value content rules as well as rules of origin.

Use of Foreign Trade Zones

When possible.

Valuation Management

Using First Sale to qualify for use of manufacturer cost as the dutiable value.

Engage with Trade Professionals

Such as customs brokers, customs law practitioners and trade consultants.

%20Market%20Overview/Tariff-Mitigating-Strategies.webp)